Every year, about 2.7 million newborns die during the first month of life.

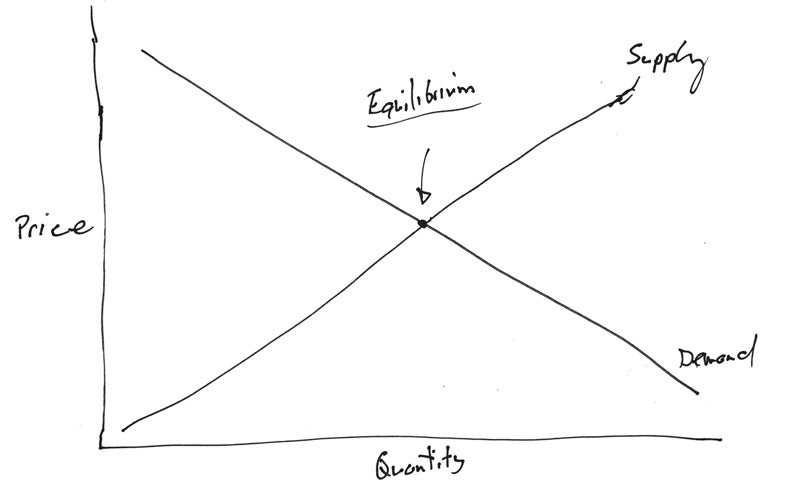

By the second semester of my freshman year at Harvard, I had started going to classes I wasn’t signed up for, and had pretty much stopped going to any of the classes I was signed up for—except for an introduction to economics class called “Ec 10.” I was fascinated by the subject, and the professor was excellent. One of the first things he taught us was the supply and demand diagram. At the time I was in college (which was longer ago than I like to admit), this was basically how the global economy worked:

There are two assumptions you can make based on this chart. The first is still more or less true today: as demand for a product goes up, supply increases, and price goes down. If the price gets too high, demand falls. The sweet spot where the two lines intersect is called equilibrium. Equilibrium is magical, because it maximizes value to society. Goods are affordable, plentiful, and profitable. Everyone wins.

The second assumption this chart makes is that the total cost of production increases as supply increases. Imagine Ford releasing a new model of car. The first car costs a bit more to create, because you have to spend money designing and testing it. But each vehicle after that requires a certain amount of materials and labor. The tenth car you build costs the same to make as the 1000thth car. The same is true for the other things that dominated the world’s economy for most of the 20 century, including agricultural products and property.

Software doesn’t work like this. Microsoft might spend a lot of money to develop the first unit of a new program, but every unit after that is virtually free to produce. Unlike the goods that powered our economy in the past, software is an intangible asset. And software isn’t the only example: data, insurance, e-books, even movies work in similar ways.

The portion of the world's economy that doesn't fit the old model just keeps getting larger. That has major implications for everything from tax law to economic policy to which cities thrive and which cities fall behind, but in general, the rules that govern the economy haven’t kept up. This is one of the biggest trends in the global economy that isn’t getting enough attention.

If you want to understand why this matters, the brilliant new book Capitalism Without Capital by Jonathan Haskel and Stian Westlake is about as good an explanation as I’ve seen. They start by defining intangible assets as “something you can’t touch.” It sounds obvious, but it’s an important distinction because intangible industries work differently than tangible industries. Products you can’t touch have a very different set of dynamics in terms of competition and risk and how you value the companies that make them.

Haskel and Westlake outline four reasons why intangible investment behaves differently:

- It’s a sunk cost. If your investment doesn’t pan out, you don’t have physical assets like machinery that you can sell off to recoup some of your money.

- It tends to create spillovers that can be taken advantage of by rival companies. Uber’s biggest strength is its network of drivers, but it’s not uncommon to meet an Uber driver who also picks up rides for Lyft.

- It’s more scalable than a physical asset. After the initial expense of the first unit, products can be replicated ad infinitum for next to nothing.

- It’s more likely to have valuable synergies with other intangible assets. Haskel and Westlake use the iPod as an example: it combined Apple’s MP3 protocol, miniaturized hard disk design, design skills, and licensing agreements with record labels.

None of these traits are inherently good or bad. They’re just different from the way manufactured goods work.

Haskel and Westlake explain all this in a straightforward way—the book is almost written like a textbook without a lot of commentary. They don’t act like there’s something evil about the trend or prescribe hard policy solutions. Instead they take the time to convince you why this transition is important and offer broad ideas about what countries can do to keep up in a world where the “Ec 10” supply and demand chart is increasingly irrelevant.

The book is eye opening, but it’s not for everyone. Although Haskel and Westlake are good about explaining things, you need some familiarity with economics to follow what they’re saying. If you’ve taken an economics course or regularly read the finance section of the Economist, however, you shouldn’t have any trouble following their arguments.

What the book reinforced for me is that lawmakers need to adjust their economic policymaking to reflect these new realities. For example, the tools many countries use to measure intangible assets are behind the times, so they’re getting an incomplete picture of the economy. The U.S. didn’t include software in GDP calculations until 1999. Even today, GDP doesn’t count investment in things like market research, branding, and training—intangible assets that companies are spending huge amounts of money on.

Measurement isn’t the only area where we’re falling behind—there are a number of big questions that lots of countries should be debating right now. Are trademark and patent laws too strict or too generous? Does competition policy need to be updated? How, if at all, should taxation policies change? What is the best way to stimulate an economy in a world where capitalism happens without the capital? We need really smart thinkers and brilliant economists digging into all of these questions. Capitalism Without Capital is the first book I’ve seen that tackles them in depth, and I think it should be required reading for policymakers.

It took time for the investment world to embrace companies built on intangible assets. In the early days of Microsoft, I felt like I was explaining something completely foreign to people. Our business plan involved a different way of looking at assets than investors were used to. They couldn’t imagine what returns we would generate over the long term.

The idea today that anyone would need to be pitched on why software is a legitimate investment seems unimaginable, but a lot has changed since the 1980s. It’s time the way we think about the economy does, too.

Badge

Badge

Badge

Badge